- Multifamily Man's Newsletter

- Posts

- Beware of Value Traps

Is NOW the time to load up on real estate at 'bargain' prices, or is the next cycle of returns bound to fall on its face? Simply put, are you buying good deals today that have a strong probability of producing mid-teen IRRs?

Multifamily prices are down 15-25% from their peak. Cap rates have expanded too. But yields are thin (often below treasury yields), and Cash-on-Cash returns are even thinner due to increasing borrowing rates. Investors are using replacement costs, diminished supply pipelines, and yesterday’s prices to rationalize today’s fair value—not a great reason to buy, in my opinion. There isn’t enough within an operator’s control to create value. To recap: everything looks like a good deal, but it isn’t actually a good deal."

This framework leads me to believe the market is primed with "value traps", where properties appear to be good investments based on traditional metrics, but in reality, they may not offer the expected returns. This shift is largely due to the hyper-financialization of the real estate market, where the focus is more on capital flows than intrinsic value. As a result, investors may find themselves making decisions based on market sentiment rather than fundamental analysis.

Understanding Value Traps

A value trap is an investment that appears to be a bargain but is actually a poor investment that underperforms the market.

In multifamily real estate, a value trap occurs when a property appears to be a bargain but has hidden issues that diminish its investment potential. These properties often have deceptively low valuation metrics, such as price per unit or high relative cap rates.

While they may initially attract investors with their seemingly low cost, these properties can reveal persistent financial instability and limited growth potential, turning what seemed like a good buy into a problematic investment.

It is important to put this concept in context across periods. Right now, most investors are still anchoring to the last 5 years of real estate performance and pricing. They suffer from a common psychological framework called recency bias - the tendency to place too much emphasis on experiences that are freshest in your memory - even if they are not the most relevant or reliable.

Investors are anchoring to peak prices. The market is down 20-30% off those prices… so everything is a deal! But in fact, many (in my humble opinion) deals are value traps.

A large portion of all multifamily bought in the past 5 years has been primarily value-add B and C class assets. The business plan was/is simple - buy a 4% cap, renovate as many units as possible in a year, collect the rent premium (moving your 4% cap to a 6% cap), and sell at a 5% cap. Now, C class real estate is trading at 6-7% caps! Prices at $60,000 - $100,000 / unit! We haven’t seen this sort of pricing in several years. But a few things have changed since then.

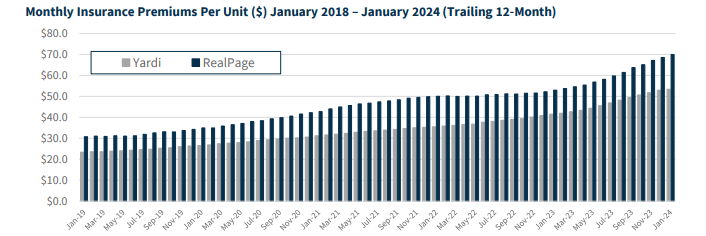

Now, operators seldom receive a justifiable premium for renovations (if there is even “meat left on the bones”) Operating Expenses have increased (primarily payroll) materially. Capital is MUCH harder to raise. All those idiotic purchases from inexperienced operators - they aren’t here anymore. In addition, your 1970’s property is now 50 years old (I know that stings if you’re coming up on the big 5-0). These types of assets take several hundred thousand dollars a year of capital to maintain, and it doesn’t show up on a P&L statement. Your cap rate and price look great, but the reality is your true Cash Yields are LOW single digits (like sub 3-4%) on the riskiest stabilized asset class in multifamily, AND you may not be able to sell to the next guy for much more than you bought it for.

Why? Because we have lost the concept of a good deal.

The Hyper-Financialization of Real Estate

How are you going to exit your investment? In real estate, the question is who is going to buy your property?

The concept of hyper-financialization refers to a market environment where capital flows and liquidity drive asset prices rather than underlying economic fundamentals. In this context, traditional measures of value, such as rental yields and occupancy rates, have taken a backseat to the availability and cost of capital.

This shift has significant implications for multifamily real estate, as investors may be more focused on the potential for capital appreciation rather than the income-generating capabilities of a property.

What happens when this framework shifts? Or fundamentals begin eroding?

At some point (which I think could be right now), there is not going to buy frothy buyers on the other side.

You, or someone, is left “holding the bag” - aka it’s your problem.

Evidence of a Value Trap

Data supports the idea that the multifamily sector is increasingly becoming a value trap. According to a report from CoStar, cap rates for multifamily properties have compressed to historically low levels, averaging around 4.5% in major markets. This compression is driven by strong demand for multifamily assets, even as rental growth has slowed. Moreover, a survey conducted by CBRE revealed that multifamily transaction volumes have remained robust, reaching over $150 billion in 2023, despite rising interest rates.

The divergence between property prices and rental income growth suggests that investors are betting on continued capital inflows rather than sustainable income generation. This scenario mirrors the dynamics described in hyper-financialized markets, where asset prices are more reflective of investor sentiment and liquidity than intrinsic value.

Investors are relying on sentiment rather than fundamentals.

The Risks of Relying on Market Sentiment

Who cares that BX, KKR, and EQR are buying portfolios of multifamily (unless you run a large AUM-driven shop). Their incentives are different than yours. Allocators are looking for safe, risk-adjusted returns relative to inflation and in context to capital demand. Capital Demand is through the roof and the big guys have to eat. Therefore, institutions are incentivized more than ever to deploy capital despite the probability of lack-luster returns.

Investors relying heavily on market sentiment and capital flows to justify multifamily investments face significant risks. Should the flow of capital into the sector slow or reverse, property values could decline, exposing investors to losses. Additionally, rising interest rates and tightening credit conditions could further exacerbate these risks, as higher financing costs may reduce the attractiveness of multifamily investments.

Who’s to say we aren’t at “return to normal” … certainly feels like it. A reliance on market sentiment can lead to herd behavior, where investors collectively drive prices up, only to see them fall when sentiment shifts. This volatility can be particularly damaging in a sector like multifamily real estate, where investments are often leveraged, amplifying the impact of price fluctuations on returns.

Stop using herd mentality as rationale to acquire.

Misleading Low Prices

CoStar Commercial Repeat-Sales Index (CCRSI) for multifamily real estate in the United States from March 1996 to March 2024

“The index measures the development of sales prices of multifamily properties, with 2000 chosen as a base year. An index value of 200 means that sales prices have doubled since 2000. In March 2024, the value-weighed index, which is more representative of the high-value deals in core markets, hit 325 index points, down from a market peak of 416 in June 2022. The equal-weighed index is more influenced by the lower-priced deals that comprise the higher share of transactions. It stood at 438 index points in March 2024, down from a market peak of 503 in June 2022 (Statista)”

What was $50,000/unit is now $175,000. Pricing as it sits today has reverted to early 2021 prices, which is right around the accelerated rent growth period. But something interesting shows up… lower-quality B/C properties are losing value quicker than Class A properties.

Part of the reason we are seeing steeper value drops in lower class multifamily is due to the asset class cap rate spread. By 2022, class A towers were trading for the same cap rates as 1980 garden styles in suburban markets despite the risk disparity. It is only natural for the risk to sort itself out. Now, core A+ located towers may trade for 4.5% caps while 80s garden in the suburbs will trade for 5.5% caps - a clear +100bp spread. The irony is that these 100 spreads is still not “good enough” because the 80s deal will have greater maintenance costs and likely a value-add component which will push true yields (on cost) equal. But there is bigger issue bubbling up in the older property space.

The biggest risk fronting multifamily today is affordability. Jay Parsons pulled comments from large REITs earnings’ calls. Here are some snippets discussing affordability - mostly in context to Class A.

Class A has clear room from the theoretical ceiling, using 33% as the “safe” RTI limit. What we don’t have as much data on is Class C operations. But we do know a few things - Bad debt is up dramatically across the board (often times in the double digits!), layoffs in the "workforce” job category as rising, and the speed at which rents have increased is far more impactful on the class C/B space. Think about it, a $200 increase on $1000 rent for someone making $40,000 annually hurts much more than a $400 increase on a $4000 rent for someone making $300,000 annually. This isn’t talked about enough right now.

Where do these rents for the next buyer? The next buyer might not be able to rationalize the “pop”, therefore they will justify a lower purchase price.

Extended Low Multiples

Prolonged periods of low valuation metrics are often a red flag for value traps. A property with a cap rate significantly higher than the local market average could signal higher risk. For instance, if the local market average cap rate is 5%, but the property is listed at an 8% cap rate, this disparity might indicate underlying problems that justify the higher perceived risk. Such properties might have structural issues, legal problems, or market disadvantages that are not immediately apparent but significantly impact their long-term viability and profitability.

Financial Instability and Growth Limitations

Multifamily properties plagued by persistent financial difficulties and limited growth potential are often value traps. Properties that do not reinvest profits into necessary improvements, maintenance, or modernization can signal trouble. For example, a property that hasn't updated its units in over a decade might struggle to attract and retain tenants, leading to lower occupancy rates and NOI. Such properties may seem stable on the surface, but their inability to compete in the market makes them vulnerable to shifts in demand and tenant preferences.

There are SO many deals that match this profile. Think about who bought all these class C/B deals over the last 5 years… inexperienced operators who are now strapped for cash. They wouldn’t even know what to address if they had the money. That means most of the capital spent through your 5 year hold period is going to be on items that will not move income - only yield downward.

Avoiding Multifamily Value Traps

To avoid falling into value traps, investors should conduct thorough due diligence:

Analyze Financials: Review the property’s financial statements, rent rolls, and maintenance records. Look for discrepancies or unusual expenses that might indicate deeper problems.

Request Historical Capital Spending: You need to see what owners have spent during there hold period.

Assess Market Conditions: Compare the property's performance to local market trends to determine if issues are property-specific or market-wide.

Evaluate Management: Investigate the history and reputation of the property management company. High turnover in management can be a red flag indicating instability and potential future problems.

The multifamily real estate market is at a critical juncture, with many properties potentially entering a value trap driven by hyper-financialization and a focus on capital flows over intrinsic value. To navigate this landscape, investors must adopt a more cautious approach, emphasizing fundamental analysis and long-term value creation. This may involve scrutinizing the income-generating potential of properties, assessing local market conditions, and being wary of overpaying in a competitive environment.

Ultimately, the key to avoiding the multifamily value trap lies in understanding the underlying drivers of asset prices and recognizing the risks associated with a market driven by capital flows rather than fundamentals.

Pay attention, and do your research!